Today’s digital wallet does not compete against other wallets. It competes against every frictionless digital experience a user has ever had — one-tap checkout, instant bank transfers, face-unlock authentication. That is the standard users bring to your onboarding screen, your payment flow, and your error messages.

The global digital payments market reached $111.1 billion in 2023 and is projected to grow at a CAGR of 15.4% through 2030, according to Grand View Research. That scale reflects a structural shift: payment infrastructure — payment rails, banking APIs, identity verification services — is now commoditized and accessible. Technology is no longer the barrier to building a digital wallet. Trust is.

Every onboarding step, balance screen, payment confirmation, and error state either builds or erodes the confidence users need to make a wallet part of their daily financial lives. This guide covers how to build that trust by design — across UX, features, security architecture, and product strategy.

A digital wallet is a software application that allows users to store, manage, and use payment credentials electronically. Instead of relying on physical cash, cards, or manual bank transfers, users can initiate and complete transactions directly through a mobile app or digital platform.

At its core, a digital wallet acts as a secure layer between users and payment systems. It enables transactions to happen quickly while reducing the friction traditionally associated with financial interactions.

Depending on the product, a digital wallet may store:

While digital wallets and banking apps are often grouped, they serve different purposes.

A banking application primarily focuses on providing access to banking services such as account management, deposits, loans, investments, and financial products. A digital wallet, on the other hand, is optimized around transactions—making it easier for users to send, receive, store, and spend money.

Today, digital wallets support a wide range of use cases:

Users can instantly transfer money to friends, family members, or contacts without needing lengthy banking details.

Wallets enable online and offline purchases through QR codes, contactless payments, or integrated checkout experiences.

Many wallets consolidate recurring payments such as utilities, internet services, subscriptions, and mobile recharges into a single experience.

Some wallets allow users to preload funds or receive credits that can be used within a specific ecosystem.

Popular digital wallet examples include Google Pay, PhonePe, Paytm, and Amazon Pay. While each product serves different customer needs, they all share the same objective: making financial transactions simpler, faster, and more accessible.

From a user’s perspective, making a payment through a digital wallet feels almost instantaneous. Behind that simple interaction, however, is a carefully orchestrated process involving multiple systems working together in real time.

A typical digital wallet transaction follows a flow similar to this:

Although this process takes only a few seconds, each stage plays a critical role in ensuring security, accuracy, and trust.

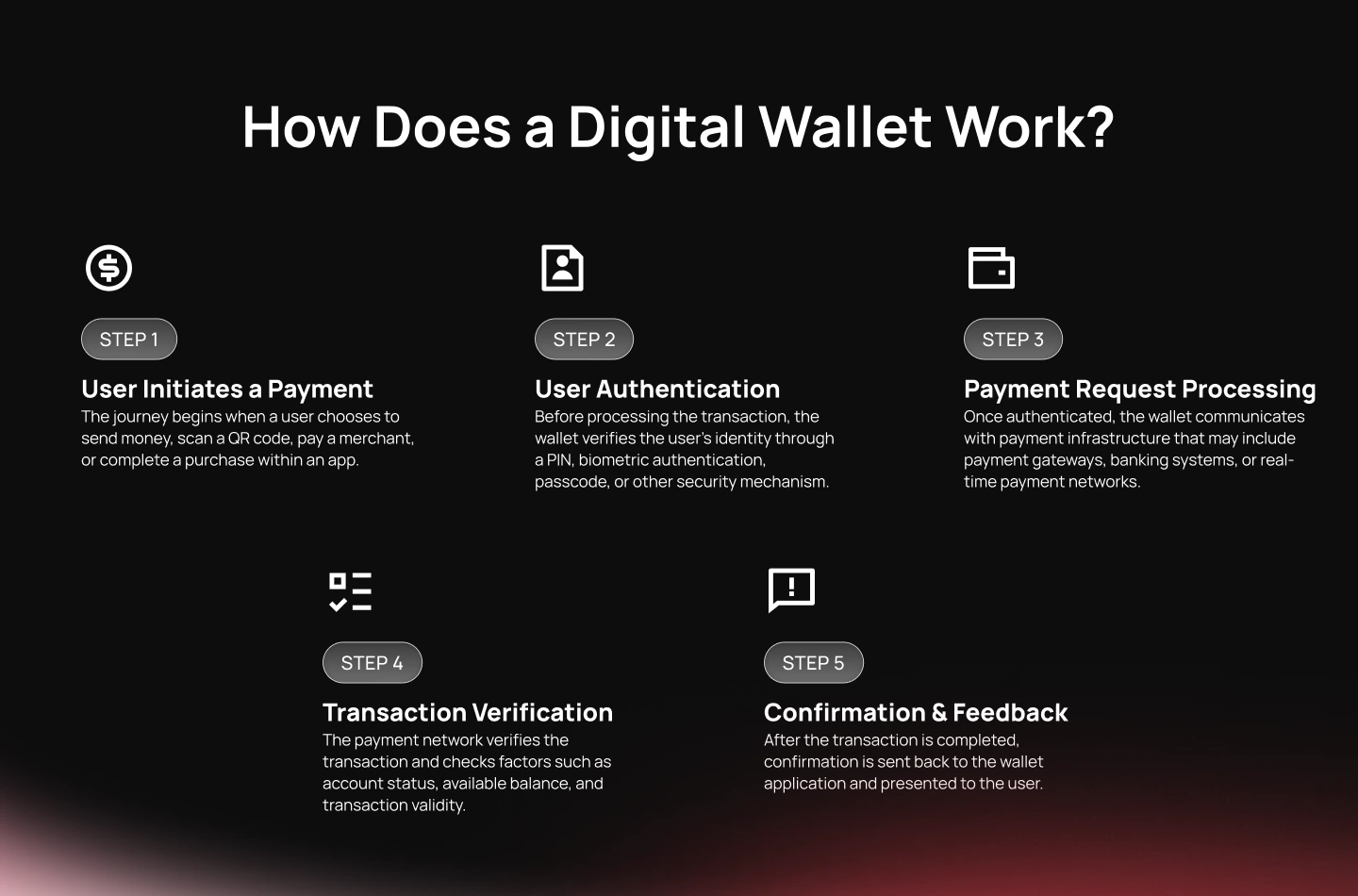

The journey begins when a user chooses to send money, scan a QR code, pay a merchant, or complete a purchase within an app.

At this stage, the wallet gathers the transaction details and prepares the payment request.

Before processing the transaction, the wallet verifies the user’s identity through a PIN, biometric authentication, passcode, or other security mechanism.

This step ensures that authorized users are initiating transactions and helps reduce fraud risk.

Once authenticated, the wallet communicates with payment infrastructure that may include payment gateways, banking systems, or real-time payment networks.

Rather than exposing sensitive financial information, modern wallets often rely on tokenization—a process that replaces sensitive payment credentials with secure digital representations.

The payment network verifies the transaction and checks factors such as account status, available balance, and transaction validity.

If approved, the transaction proceeds through the relevant banking or payment systems.

After the transaction is completed, confirmation is sent back to the wallet application and presented to the user.

This final step may seem straightforward, but it is one of the most important moments in the user journey. A clear confirmation screen reassures users that their money has reached the intended destination.

From a UX perspective, every stage influences the overall experience. Slow response times create uncertainty. Poorly explained errors increase support requests.

Unclear transaction states reduce trust. Successful digital wallet products recognize that users are not evaluating the underlying payment infrastructure—they are evaluating how confidently and effortlessly they can complete a transaction. That is why UX design must be considered alongside payment architecture from the very beginning.

Not all digital wallets are designed to solve the same problem. The structure of a wallet influences everything from compliance requirements and transaction flows to onboarding complexity and user expectations.

Understanding the different types of digital wallets is an important step when determining how to create a digital wallet that aligns with both business objectives and customer needs.

A closed wallet is designed for use within a single brand or ecosystem. Users can store funds, credits, refunds, or rewards and spend them exclusively with the issuing business. These wallets are commonly used by e-commerce platforms, retailers, and service providers looking to increase retention and encourage repeat purchases.

Because transactions remain within a controlled ecosystem, closed wallets often have simpler payment journeys and a more focused feature set.

Semi-closed wallets are accepted across a network of participating merchants. This is one of the most widely adopted wallet models because it balances flexibility for users with manageable operational complexity for providers.

Users can make payments, transfer funds, and complete transactions across multiple merchants without needing direct access to banking services within the wallet itself.

Designing for semi-closed wallets requires greater attention to merchant discovery, transaction transparency, and support experiences because users interact with a broader ecosystem.

Open wallets offer the highest degree of interoperability. Typically supported through partnerships with regulated financial institutions, these wallets allow users to transact across a wider range of payment environments and financial services.

Open wallets often support additional use cases such as bank transfers, cash withdrawals, and more extensive payment capabilities. As functionality expands, so does the importance of security, onboarding, authentication, and compliance-focused user experiences.

Features are not what makes a digital wallet successful. Reducing the cognitive effort required to use them is. The most trusted wallets are not the ones with the longest feature lists — they are the ones where every capability feels obvious, fast, and safe. With that standard in mind, here are the eight features every digital wallet must get right:

The first impression of trust. Balance compliance requirements (mobile number verification, KYC, progressive information collection) with minimal friction. Every unnecessary form field reduces activation rates. The goal is to get users to their first transaction as quickly as compliance allows.

Users must be able to connect funding sources quickly and confidently.

Whether linking a bank account, connecting a payment method, or enabling account transfers, the experience should communicate status clearly at every stage.

Key considerations include:

Many wallet experiences lose users at this stage because the process feels overly technical or uncertain.

For many users, this is the core reason the wallet exists. The experience should prioritize speed, clarity, and confidence. Common capabilities include:

Reducing cognitive effort is often more valuable than adding additional functionality. Users should never need to think twice about where money is being sent or what happens after they tap “Pay.”

As wallets evolve, recurring financial activities become an important retention driver.

Allowing users to manage regular payments from a single interface creates convenience while encouraging habitual engagement.

Useful features include:

These experiences transform the wallet from a transaction tool into an ongoing financial utility.

Users frequently revisit transaction records to verify payments, resolve disputes, or monitor spending.

A transaction history should function as a source of clarity rather than a list of records.

Important elements include:

Clear labeling becomes especially important when transactions are pending, delayed, or reversed.

Modern wallet experiences increasingly help users understand their financial behavior. Simple spending summaries and balance visibility can improve engagement while helping users feel more in control of their finances.

Useful features may include:

The goal is not to replicate a personal finance application but to provide meaningful context around wallet usage.

Financial products depend heavily on timely communication. Notifications help users stay informed while reinforcing trust in the platform.

Common examples include:

Every notification should answer a simple question: “What happened, and what should I do next?”

Security features should be integrated into the experience rather than treated as isolated checkpoints.

Common authentication methods include:

The best experiences adapt authentication requirements based on transaction context and risk levels rather than applying the same level of friction to every interaction.

The difference between a functional wallet and a trusted wallet is rarely technical. More often, it comes down to how the experience makes users feel. Money is inherently emotional. Users expect accuracy, transparency, and control whenever they interact with financial products. Even small moments of uncertainty can undermine trust.

For this reason, digital wallet UX should not be viewed as a visual design exercise. It is a trust-building system that supports every financial interaction.

Users continuously evaluate whether they can trust a wallet. Most trust signals are formed through interface decisions rather than explicit messaging. Throughout every transaction journey, users are trying to answer three questions:

Convenience is the primary reason users adopt a digital wallet over a traditional payment method. Every step added to a payment flow is a point of potential abandonment — and the cumulative effect of small friction moments determines whether users build a habit or quietly switch to a competitor.

The goal of payment flow design is not speed alone. It is minimizing the total effort required to complete a transaction successfully. The highest-leverage design decisions are:

The most trusted payment experiences feel invisible — users are focused entirely on the outcome, not on operating the interface. Apple Pay’s face-unlock-to-confirmation flow is the benchmark: one deliberate action, one immediate result, zero ambiguity.

Payment failures are among the most important moments in a wallet experience. Interestingly, users often remember failed payments more vividly than successful ones. When something goes wrong, uncertainty increases rapidly. Questions such as: “Was I charged? Did the payment go through? Will I get my money back?” can create significant anxiety. Strong failure-state design addresses these concerns proactively.

Avoid generic error messages. Users need simple, clear explanations to understand what went wrong. The app should show the current status immediately and clearly separate these transaction states: Processing, Pending, Successful, Failed, and Refund. This helps users always know what is happening with their money and feel safe.

The interface should guide users toward the next appropriate action. Retrying, contacting support, checking account balances, or waiting for processing should all be communicated clearly.

If refunds are involved, visibility becomes critical. Users should understand the expected timeline and current status without needing to contact support.

A wallet’s ability to handle failure gracefully is often a stronger trust signal than its ability to process successful payments.

The first transaction frequently determines whether a user becomes an active customer or abandons the product. New users should be guided toward activation without feeling overwhelmed by features. Effective onboarding experiences typically prioritize:

Feature discovery can happen later. Activation should come first.

Empty states, contextual guidance, and progressive education help users understand value at the moment it becomes relevant rather than forcing them to learn everything upfront.

The most successful digital wallets create momentum early, helping users experience value before introducing complexity.

Security is often discussed as a technical requirement, but in reality, it is also a user experience challenge.

A wallet can implement sophisticated security measures behind the scenes, but if users do not understand or trust those protections, adoption suffers. Conversely, overly aggressive security measures can create friction that discourages usage.

The most successful digital wallet products strike a balance between protection and convenience, ensuring that security feels reassuring rather than obstructive.

One of the most important security mechanisms in modern payment systems is tokenization.

Instead of storing or transmitting sensitive payment credentials directly, tokenization replaces them with unique digital tokens that can be used to authorize transactions. This approach significantly reduces the risk associated with data exposure because the underlying payment information remains protected even if a token is intercepted.

For users, tokenization is largely invisible. However, it plays a critical role in creating secure payment experiences while enabling fast and seamless transactions.

Digital wallets handle highly sensitive information, including personal details, payment credentials, transaction records, and account information. Protecting this data requires strong encryption practices across the entire system.

Security measures typically include:

While users may never see these protections directly, they form the foundation of trust within any financial product.

Authentication is one of the most visible security interactions users encounter. Modern wallets often combine multiple verification methods to strengthen account protection while maintaining convenience.

Common approaches include:

Rather than applying the same level of security to every interaction, leading products increasingly use risk-based authentication models that adjust protection according to context. Checking a balance may require minimal friction. Transferring a significant amount of money may require additional verification.

This adaptive approach improves both security and usability.

Digital wallet providers must continuously monitor for suspicious activity. Fraud prevention systems often evaluate factors such as:

The goal is not simply to stop fraud. It is to identify risk without creating unnecessary barriers for legitimate users.

From a UX perspective, security interventions should feel proportionate and explainable. Users are more likely to trust security measures when they understand why additional verification is required.

Compliance requirements vary across markets, wallet types, and regulatory environments.

While specific obligations differ, most digital wallet providers must consider areas such as:

Compliance should not be treated as a final-stage requirement. It influences onboarding design, account management flows, transaction experiences, and data handling practices from the earliest stages of product development.

Behind every digital wallet is a network of systems working together to deliver secure, reliable, and near-instant financial interactions.

While end users may never see this infrastructure, its performance directly impacts the quality of the product experience.

When discussing digital wallet app development, it is helpful to think of APIs not simply as technical integrations but as experience enablers. Every API influences how quickly users can complete actions, receive confirmations, and trust the platform.

Payment APIs facilitate the movement of money between users, merchants, and financial institutions. They support core wallet functions such as:

From a UX perspective, payment APIs influence transaction speed, reliability, and user confidence.

A payment that feels slow often feels less trustworthy, even when it eventually succeeds.

Identity verification services support onboarding and compliance workflows. These integrations help verify user information and streamline account creation processes. Their impact extends beyond compliance.

Poorly designed verification experiences can significantly increase onboarding abandonment rates.

Effective wallet experiences minimize user effort while maintaining necessary verification standards.

Many wallets require access to financial accounts and related services. Banking connectivity APIs support functions such as:

These integrations help create connected financial experiences while reducing manual data entry. The smoother the connection process, the faster users can begin transacting.

Real-time communication is critical in financial products. Notification infrastructure supports:

Every notification reinforces trust by helping users understand what has happened and whether further action is required.

Risk management systems help identify suspicious behavior before transactions are completed.

These tools support:

The challenge lies in applying these protections without creating unnecessary friction for legitimate users.

Many product teams underestimate the relationship between infrastructure and experience.

In reality, API performance directly affects:

A well-designed interface cannot compensate for unreliable infrastructure.

Likewise, strong infrastructure can become invisible when paired with thoughtful UX design.

The most successful digital wallets treat experience design and technical architecture as interconnected disciplines rather than separate workstreams.

Creating a digital wallet is not simply a technology initiative—it is an exercise in building trust at scale.

The products that succeed are not necessarily those with the longest feature lists or the most complex infrastructure. They are the ones that help users feel confident, informed, and in control throughout every interaction.

From onboarding and authentication to transaction confirmations and failure recovery, every touchpoint contributes to the perception of trust. Security, usability, and product strategy must work together to create experiences that users are willing to adopt as part of their daily financial lives.

As digital payments continue to evolve, the most effective wallet experiences will be those that balance convenience with confidence, reducing complexity while maintaining transparency at every step.

At Lollypop, we help organizations design fintech products that users trust—from defining product strategy and user journeys to creating scalable digital experiences that support long-term growth. Planning your digital wallet? Let’s design it the right way together. Ready to transform your product? Explore our fintech design expertise to see how we can help.

A digital wallet stores and manages payment credentials in a secure digital environment. When a user initiates a transaction, the wallet authenticates the user, communicates with payment infrastructure, processes the payment through relevant financial systems, and provides confirmation once the transaction is completed. Modern wallets use technologies such as tokenization and encryption to protect sensitive information throughout the process.

Core digital wallet features typically include user onboarding, identity verification, account linking, money transfers, bill payments, transaction history, notifications, and authentication mechanisms. Additional features may include spending insights, rewards programs, recurring payments, and personalized financial experiences depending on the product’s objectives.

Digital wallets can provide a highly secure payment experience when built using established security practices. Common protections include tokenization, encryption, multi-factor authentication, fraud monitoring, and risk-based security controls. User trust depends on both technical security measures and clear communication throughout the transaction experience.